As of mid‑2026, the global memory market is in one of the sharpest price upswings in its history, with contract prices for DRAM and NAND flash surging quarter after quarter and no clear sign of relief. What started as a gradual recovery cycle in late 2024 has turned into a full‑blown “super‑cycle,” driven primarily by insatiable demand from artificial intelligence (AI) data centers and high‑bandwidth memory (HBM) attached to AI accelerators. (Source: TrendForce, CNBC)

DRAM and NAND Prices Are Climbing at Record Pace

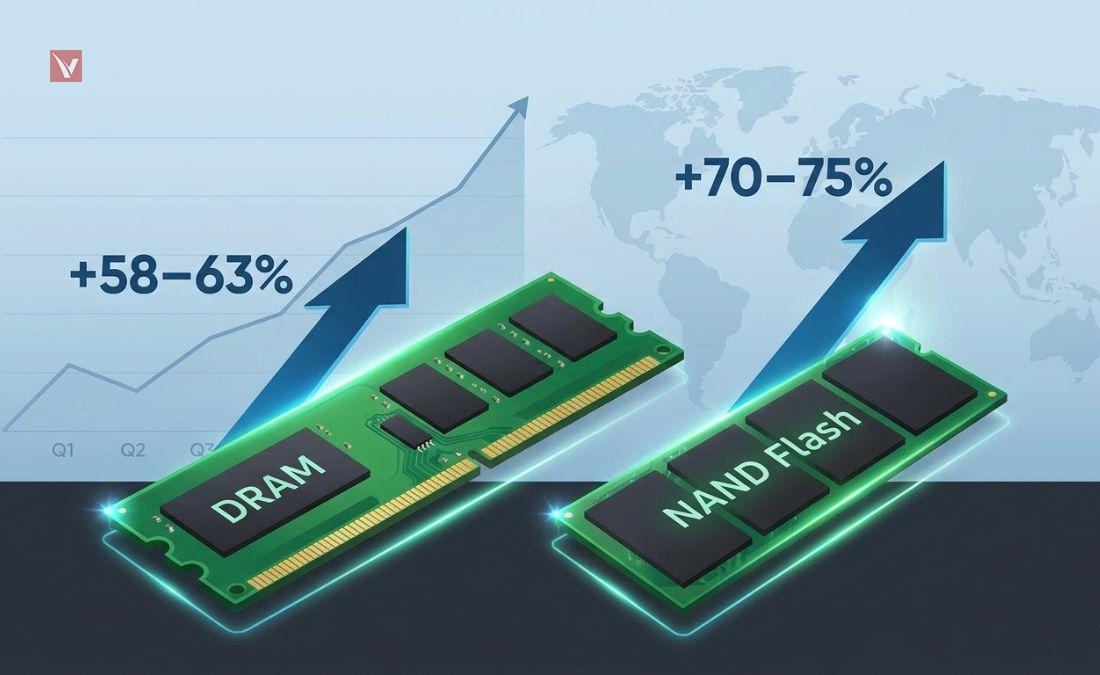

Market research firm TrendForce now expects conventional DRAM contract prices to rise by 58% to 63% quarter‑on‑quarter in the second quarter of 2026, while NAND flash contract prices are forecast to jump by a staggering 70% to 75% over the same period. These increases come on top of an already extraordinary first quarter, where revised projections indicated that DRAM prices could climb by 90% to 95% compared with the final quarter of 2025, with NAND prices up by 55% to 60%.

TrendForce’s latest industry survey also shows that this rapid price escalation has significantly boosted overall DRAM industry revenue, which grew 81% quarter‑on‑quarter in the first quarter of 2026 to around 97 billion US dollars. In short, memory is no longer a cheap, commoditized afterthought in system design; it has become one of the most volatile and strategic components in the entire semiconductor stack.

AI Data Centers Are Absorbing Global Memory Supply

The core driver of this price shock is not traditional PCs or smartphones but the rapid build‑out of AI infrastructure. Cloud providers and AI companies are racing to deploy clusters of GPUs and AI accelerators, each node often configured with hundreds of gigabytes of DRAM and multiple stacks of HBM, dramatically increasing memory intensity per server compared with classic cloud workloads. (Source: CNBC, TrendForce)

Reports from major US media describe AI giants “gobbling up” memory chips and effectively sitting at the front of the allocation queue. Companies such as Alphabet, OpenAI, and other hyperscalers are committing to long‑term supply agreements that tie up a large portion of DRAM and advanced HBM capacity, leaving consumer‑oriented device makers competing for a shrinking pool of available chips from suppliers like Samsung, SK hynix, and Micron.

As a result, what began as a tight market for premium AI memory has spilled over into conventional server DRAM, PC DRAM, and mobile LPDDR, pushing prices higher across almost every major segment.

Capacity Is Being Reallocated Toward High‑Margin AI Products

A key reason price increases have been so steep is that memory manufacturers are deliberately reallocating capacity toward higher‑margin AI products rather than simply ramping output across the board. Analysts note that suppliers are shifting production from legacy or mainstream products toward advanced nodes and HBM, since these deliver much better profitability per wafer under current market conditions.

This strategic pivot has created what some commentators call an “artificial scarcity” in traditional DRAM and NAND used in PCs, smartphones, and embedded systems. Even though overall wafer starts may not have collapsed, the mix has changed in favor of AI‑oriented products, effectively constraining supply for mass‑market memory and giving suppliers stronger pricing power.

The market has therefore moved into a clear seller‑dominated phase, where buyers face not only higher prices but also longer lead times and stricter allocation.

Downstream Devices Are Facing Cost Pressure

The impact of this memory squeeze is now radiating throughout the electronics ecosystem. PC OEMs and notebook brands are warning of higher bill‑of‑materials (BOM) costs, while some smartphone vendors are signaling that device prices may have to rise or memory configurations be reduced to protect margins.

Industry analysts expect average smartphone selling prices to climb to record levels in 2026 as memory and other semiconductor components become more expensive. (Source: CNN) Similarly, PC DRAM prices are projected to more than double in some configurations for the first quarter of 2026, increasing cost pressure on consumer and commercial systems alike.

For electronics manufacturers, this shift is forcing a range of tactical responses: redesigning product SKUs with lower memory capacity, delaying launches that rely heavily on high‑end configurations, or renegotiating long‑term supply contracts to gain better visibility on pricing.

A “Super‑Cycle” Rather Than a Short‑Term Spike

What makes the current environment particularly challenging is that many experts no longer see this as a short‑lived spike but as part of a longer “super‑cycle” underpinned by structural AI demand. Reports from financial and industry media highlight that DRAM and NAND prices have already risen several‑fold from their 2025 lows, and key investment banks now forecast that average selling prices could continue to climb through the remainder of 2026.

According to some forecasts, DRAM average selling prices in 2026 could be nearly double those of the previous year, while NAND prices may see similarly outsized gains as capacity remains constrained and AI workloads proliferate. In parallel, TrendForce’s latest numbers suggest that even “conventional” DRAM—rather than only HBM—will maintain strong pricing momentum due to persistent shortages.

This combination of AI‑driven demand, cautious capacity expansions and ongoing inventory discipline by suppliers is what underpins the narrative of a multi‑year upswing rather than a brief boom‑and‑bust cycle.

What Buyers and OEMs Should Watch Next

For buyers of memory and procurement teams across electronics, several trends deserve close attention over the next few quarters. First, as more hyperscalers lock in long‑term HBM and DRAM supply, spot market volatility for the remaining volume may even increase, making it harder for smaller OEMs to source at reasonable prices.

Second, a significant share of incremental capacity investments from major players like Samsung, SK hynix and Micron is still focused on advanced nodes and AI‑centric products, meaning there is limited near‑term relief for standard DRAM and mid‑range NAND segments. Third, any macroeconomic slowdown might cool end‑device demand but is unlikely, at least initially, to dampen AI infrastructure build‑outs, which are driven by strategic and competitive pressures rather than just short‑term consumer demand.

For now, industry observers broadly agree that 2026 will remain a difficult year for buyers but a highly profitable one for memory suppliers, with AI continuing to “empty the warehouse” of available DRAM and NAND across the globe.